EURW on Monad: Everything You Need to Know

2026-05-07

We recently joined the Monad morning show for a live AMA so the community could ask any questions they had about Newrails, EURW and the Monad launch.

This article covers all the key topics discussed, including what Newrails is building and why, the regulatory environment in which we operate, how stablecoins compare to traditional banking and what the future holds.

What is Newrails and what are you building?

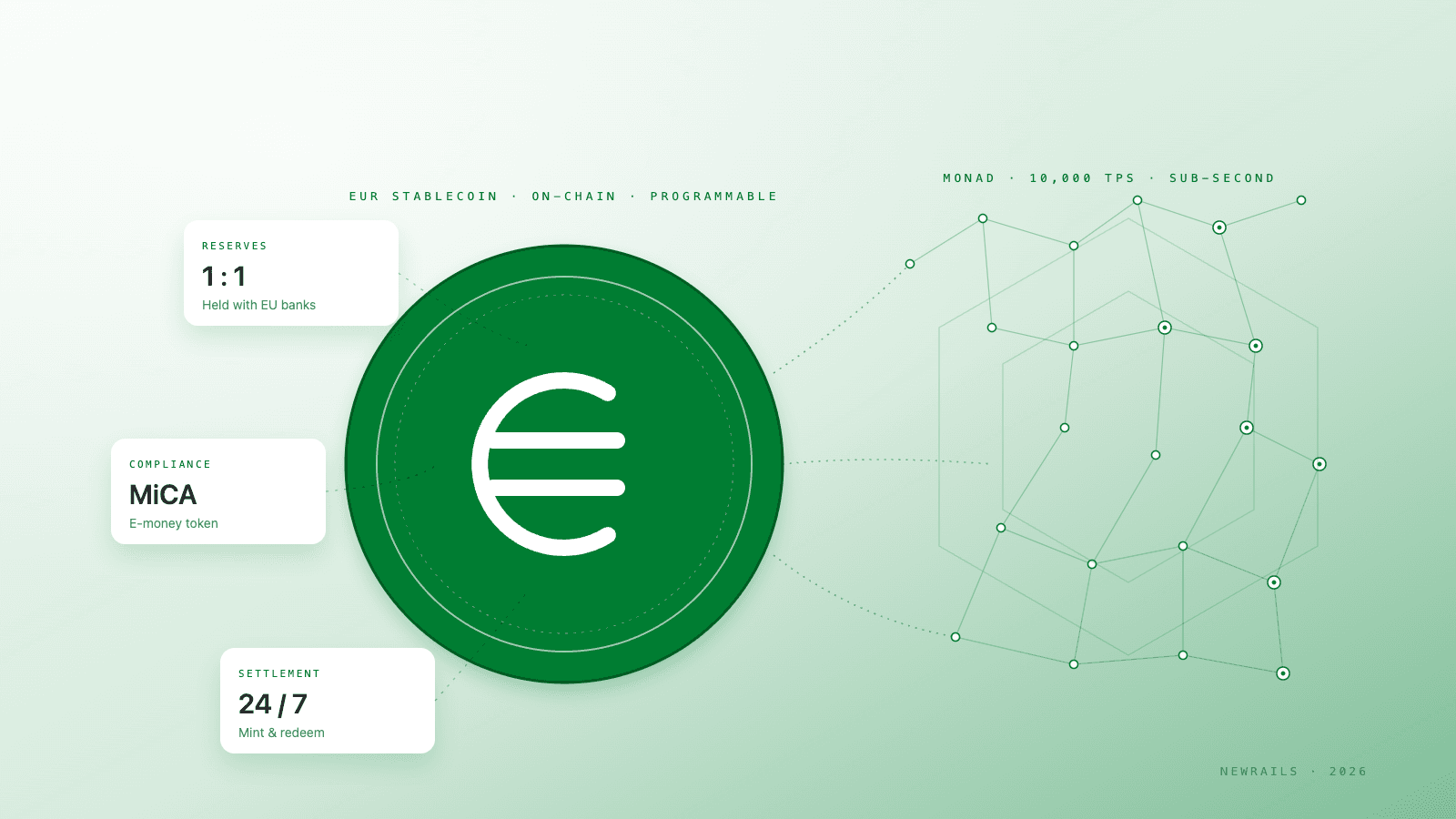

Newrails is a regulated fintech and stablecoin infrastructure company focused on building the next generation of cross-border payments and settlement. The mission is to combine regulated Euro banking with stablecoin technology to create a new payment infrastructure that enables instant settlement, programmable money and fair global access.

What makes Newrails different from other stablecoin issuers is its scope. Issuing a stablecoin is one thing but building the accounts, rails, and real-world use cases around it is another. This is where Newrails is focused, with the Euro-backed stablecoin, EURW, as the foundation and the banking and payments network built around it.

Why the focus on stablecoins?

The world is beginning to recognise stablecoins as real money rather than a form of crypto. That distinction is significant. Crypto has largely been associated with speculation but money is about the flow of value.

When governments and regulators start recognising stablecoins as a legitimate new form of money capable of facilitating economic growth, that is a tipping point. That is the moment mass adoption becomes possible, beyond DeFi enthusiasts and early adopters. Newrails is perpefectly positioned to take advantage of this opportunity.

What can you tell us about the use cases Newrails serves?

The core customer at this early stage is the cross-border merchant.

Consider what international trade currently looks like for a business operating between Hong Kong and Europe, for example. They need to open a bank account, which involves passing Know-Your-Business (KYB) and Know-Your-Customer (KYC) checks that many international businesses struggle with.

Then, when they send or receive money, they go through SWIFT, which takes T+2 or T+3 days and carries significant Foreign Exchange (FX) fees. It is slow and expensive.

Newrails addresses this directly by enabling all international businesses, not just European ones, to open a Euro bank account to receive and send money. Their experience is made easier because of the access they have to the EURW stablecoin, which settles quickly and around the clock, unlike traditional banking. On Monad, FX conversions happen via liquidity pools that enable efficient conversion at low cost.

The payment corridors Newrails plans to build from Europe to Hong Kong, Latam and Africa is where we see the most immediate and real demand, all without touching traditional rails.

It’s important to note that the merchant who simply wants cheaper, faster international payments and has no interest in the crypto does not need to interact with that infrastructure. They just see Euros in and Euros out, as they need.

Another interesting use case is one involving treasury-focused businesses that actively want to be on-chain and earning yield by providing liquidity or using DeFi protocols. In this case, Newrails acts as the underlying collateral layer for lending, borrowing and staking across DeFi. We are also building API access for developers to integrate these services directly into their own products.

Both use cases are real and operate in parallel.

Why did Newrails launch on Monad?

The three main reasons for launching on Monad are performance, ecosystem and alignment.

On performance, Monad is fast, cheap and built for large-scale transactions, which is exactly what cross-border payments infrastructure requires. In terms of the ecosystem, the Monad community is active and growing, while the team is collaborative rather than transactional.

On alignment, the Monad team understands payments at a deep level. They are not simply looking to establish a high Total Value Locked (TVL) for assets on-chain. They understand that Newrails and EURW have real-world payment use cases and are genuinely interested in supporting us.

That kind of strategic alignment matters when building infrastructure that needs to work for non-crypto users as much as for on-chain ones.

What can you tell us about Newrails' licensing in Europe?

Newrails operates under MiCA, the EU's Markets in Crypto Assets regulation. We are also licensed in Lithuania, with reporting obligations to both the Lithuanian central bank.

In practice, MiCA is strict. Reserves must be maintained one-to-one at all times and backed by auditing reports. Redemption must be available instantly and at zero cost. All policies must be fully transparent and publicly available. The compliance burden is significant and this creates a high barrier to entry, which means only qualified institutions can issue Euro stablecoins.

For users, this matters. Someone who has never used stablecoin before can look at a MiCA-regulated stablecoin and see something that operates by rules they can understand and trust, similar to a bank. That credibility is essential for broadening the audience for stablecoins beyond those already comfortable with crypto.

What does Newrails offer that the traditional system cannot?

The contrast in terms of cost is substantial.

For low and medium-risk clients, Newrails charges near-zero fees, so effectively free in most cases. Minting and redeeming EURW currently carries no fee. FX conversion is priced between 0.05% and 0.1%, and will improve further as liquidity grows.

By comparison, retail conversion through traditional or crypto routes can cost around 1%. One reason for our low fees is that Newrails is directly integrated with CENTROlink, the central bank clearing system, which enables the lowest costs across fiat and crypto rails.

On the broader question of banks versus stablecoins, the trajectory is clear. Banks currently weigh stablecoin compliance costs as too high relative to the reward.

However, that calculation is starting to change. Anti-Money Laundering (AML) tools are improving, transaction monitoring is becoming more sophisticated and it is increasingly difficult to use stablecoins for illicit activity. As the risk reduces, banks become more open.

Plus, some banks are already there or getting there. But this transition period is exactly where payment institutions can move fastest, by building the infrastructure, demonstrating the controls and showing that the risk is manageable.

The pitch to banks is straightforward: the rewards are growing, the risks are reducing and the regulatory framework is clear. Stablecoin adoption is a global trend that won’t be derailed by a single institution or country opting out. So why wait?

What does the future hold for Newrails and stablecoins?

The immediate focus is building out direct currency corridors on Monad, like Euro to Turkish Lira, Euro to Nigerian Naira and Euro to Hong Kong Dollar. The goal is end-to-end merchant payment flows, region by region, that businesses can use without thinking about crypto.

This matters because today, most international payments outside USD pairs still route through SWIFT, which involves converting into USD and then converting back. Every conversion adds cost and time. Direct on-chain currency pairs remove that friction entirely and open up FX fee earning to anyone providing liquidity in those pools.

The broader momentum supports this direction. Visa and Mastercard are already integrating stablecoins. Banking rails in Europe are connecting with stablecoin issuers. Institutional adoption is no longer a prediction; it is underway. The infrastructure being built now is what future mass adoption will run on.